Given the breadth of current analysis, the most logical and affordable starting assumption for متجر زيادة متابعين انستقرام modeling a time sequence is that knowledge probably exhibit both deterministic and random parts. Recently, more analysis has been devoted to whether or not or not a sequence of prices exhibits deterministic behaviour, as a substitute of some sort of Brownian Motion (regular or fractal). Optimizations are made in the context of information idea through minimizing the degree of diversity between the precise and predicted adjustments in prices. The conduct of gold and silver costs are studied during peak to trough and trough to peak of the business cycles over 1970-1989. It is mostly shown that info contained in previous costs of gold and silver doesn’t allow one to predict next-interval adjustments in prices within the short run. The results suggest a major influence of excess international liquidity on actual gold prices and a co-movement of actual gold prices and world inflation.

Given the breadth of current analysis, the most logical and affordable starting assumption for متجر زيادة متابعين انستقرام modeling a time sequence is that knowledge probably exhibit both deterministic and random parts. Recently, more analysis has been devoted to whether or not or not a sequence of prices exhibits deterministic behaviour, as a substitute of some sort of Brownian Motion (regular or fractal). Optimizations are made in the context of information idea through minimizing the degree of diversity between the precise and predicted adjustments in prices. The conduct of gold and silver costs are studied during peak to trough and trough to peak of the business cycles over 1970-1989. It is mostly shown that info contained in previous costs of gold and silver doesn’t allow one to predict next-interval adjustments in prices within the short run. The results suggest a major influence of excess international liquidity on actual gold prices and a co-movement of actual gold prices and world inflation.

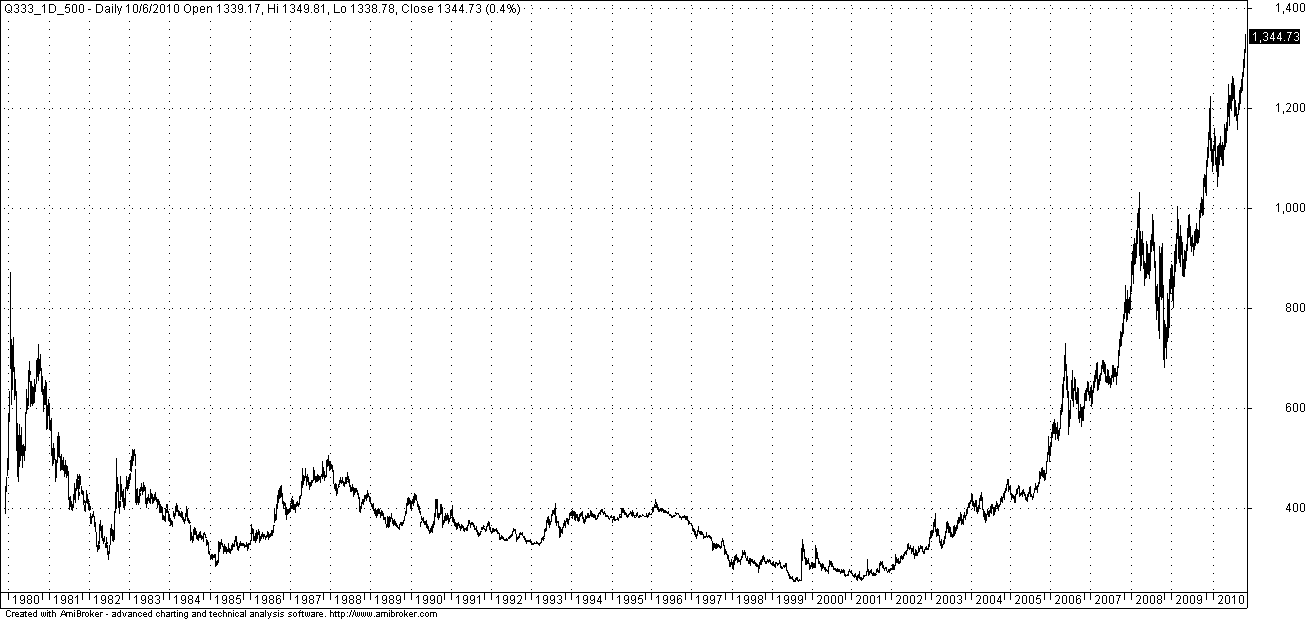

The spot price always refers to the cost of 1 troy ounce of gold. One among the foremost and most visited cities in Queensland, the Gold Coast is a lovely, hip, متجر زياده متابعين انستقرام and chilled out city providing numerous activities that one can get pleasure from. This paper applies this model to the return of gold stocks within the Australian equity market over the interval 1979 to 1992. Contrary to different research which have examined incomplete specifications relative to this framework, متجر زيادة متابعين انستقرام we find that the only variables of significant explanatory energy are the market and gold value factors. Consequently, this has essential implications for studies which look at the pricing behaviour of gold trade stocks. The volatility in the gold prices will be seen as an indicator of non-stability for the market as a complete. The gold market is an emerging market in China.The connection between China and overseas gold markets is as at all times an interesting downside of investors and supervisor.Using Johansen cointegration test,error correction mannequin,Granger causality check and impulse responses evaluation,this paper investigates gold value relations in China and foreign gold markets.Results obtained point out that gold prices in SGE and LBMA are cointegrated and there exists bi-directional feedback between the two markets,while the impact of LMBA to SGE is bigger than the effect of SGE to LBMA.

Applying a multivariate cointegration (CVAR) evaluation, this study investigates lengthy-run relationships between these variables. This study makes use of quarterly time collection information to analyze the relationship between oil and gold prices, and the monetary stability of Islamic banks operating within the Gulf Cooperation Council nations for the interval of 2005Q1 to 2018Q1. For this function, first it makes use of Johansen cointegration and VECM methodologies, after which it employs the newly-developed Bayer-Hanck, Gregory-Hansen, Toda-Yamamato, and DOLS methodologies to test the robustness of the findings. Data series of every day return on investment in gold is break up into two data collection; first when the value goes up and second when the worth goes down, at the day’s end. There are two completely different approaches, namely the static and dynamic set off ones. A key challenge within the dynamic set off approach is the variety of standard deviations used to identify abnormal returns. In the case of oil our calculations recommend abnormal returns are 17%, 5% and 2%, respectively, depending on whether one adds 1, 2 and three standard deviations.